Fixed rate end date

Check when your current fixed rate period is due to finish.

Add your fixed-rate end date and Onremind will remind you before it ends, so you have time to review your lender’s options, speak to a broker and plan before the follow-on rate becomes the default.

We remind you in good time, so you have time to act.

Check, switch, cancel or stay before it is too late.

We never access your bank or personal accounts.

Onremind is impartial and not affiliated to any provider.

Before the fixed rate ends

Your fixed rate mortgage end date is the point where your current fixed rate period may finish. After that date, your mortgage may move to another rate or payment position.

The useful moment is before the fixed rate end date, while you still have time to check what happens next and decide what to do.

Check when your current fixed rate period is due to finish.

Check what rate or payment position may apply after the fixed rate ends.

Check whether your monthly mortgage payment may change after the fixed rate period ends.

Check when to speak to your lender, broker or adviser before the fixed rate ends.

Check whether any product fees, exit fees or early repayment charges may affect your review timing.

Check your mortgage offer, account information and any messages from your lender before the end date.

Onremind warns before the date so you have time to review the fixed rate end date, follow-on rate position, monthly payment, lender or broker timing, fees and documents.

You do not have to make the decision on the fixed rate end date.

Add the date early, then review before the window closes.

Add the date once. Onremind tracks the countdown, reminds you early, and gives you time to review, negotiate, cancel, switch or stay before the renewal date arrives.

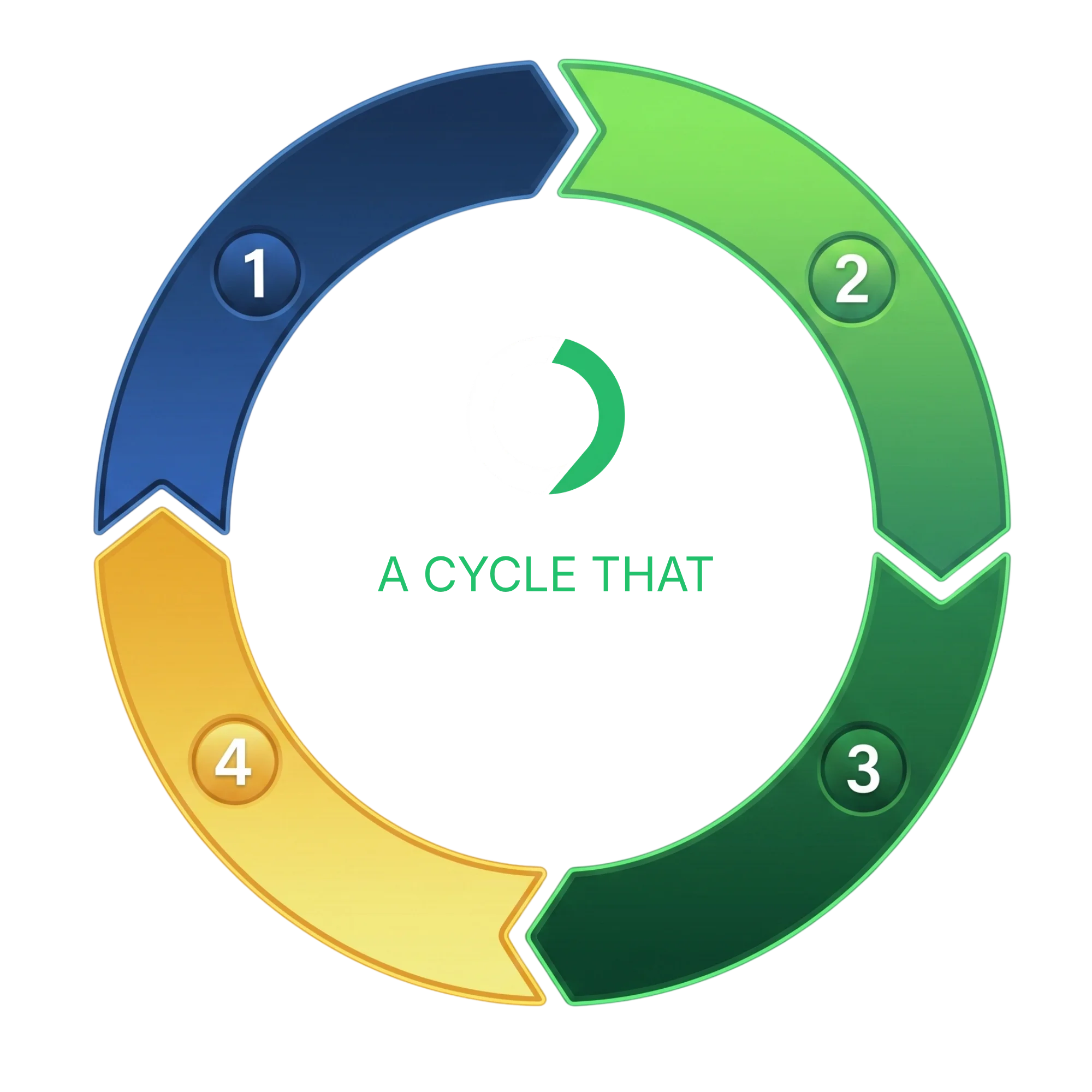

Add the renewal, expiry or contract-end date once.

Sit back. We quietly track the countdown for you.

We remind you while there's still time to review and decide.

The renewal, expiry or contract-end date is reached.

Then the cycle begins again.

Add the renewal, expiry or contract-end date once.

Sit back. We quietly track the countdown for you.

We remind you while there's still time to review and decide.

The renewal, expiry or contract-end date is reached.

Then the cycle begins again.

Add the renewal, expiry or contract-end date once.

Sit back. We quietly track the countdown for you.

We remind you while there's still time to review and decide.

The renewal, expiry or contract-end date is reached.

Then the cycle begins again.

The renewal date is the trigger. The renewal action window is the time Onremind protects.

Renewal resources

These pages support the same decision point from three angles: fixed-rate evidence, practical timing guidance and current developments that may affect how you review before your fixed rate ends.

Research on fixed rate mortgage endings, follow-on rate risk and why mortgage holders should review before the fixed rate end date.

Practical guidance on fixed rate end dates, follow-on rate position, payment changes and what to check before the fixed period ends.

A clear summary of FCA remortgage rule changes and what they may mean before your fixed rate mortgage ends.

More mortgage dates

A fixed rate end date is one mortgage timing point. Onremind can also help you track a remortgage review date before your current deal ends.

Track a review date before your fixed rate ends so you have time to check what happens next.

Remortgage reminderMortgage questions

Quick answers to common questions about fixed rate mortgage end dates, follow-on rates, monthly payments and what to check before the fixed period ends.

We'll remind you before the date needs review.