Credit card costs can change when promotional rates end.

Add dates for 0% periods and balance transfers. Onremind reminds you before the promotional rate ends, so you have time to review the remaining balance before standard interest can apply.

Credit card deals we help protect

How Onremind works

- 1

Add the renewal date

Enter when your policy renews.

- 2

We track the countdown

Onremind keeps watch in the background.

- 3

We remind you early

You get warning before the date arrives.

- 4

You choose what to do

Review, cancel, negotiate, switch or stay.

- 5

Log the result

Record what happened and what you avoided.

Onremind protects your moment to choose.

Get reminded early

We remind you in good time, so you have time to act.

Save time and money

Check, switch, cancel or stay before it is too late.

Privacy first

We never access your bank or personal accounts.

Independent reminder system

Onremind is impartial and not affiliated to any provider.

How credit card offer endings typically work

Credit card offers can sit quietly in the background. When the offer date passes, interest may apply before you have reviewed what to do next.

How a credit card offer ending works

1.A 0% or balance transfer offer starts

The card gives you a promotional period that runs until a fixed end date.

2.The end date approaches

Before the offer ends, you need time to review the balance and decide what to do.

3.Interest may apply

If the offer ends before you act, interest can start applying to the remaining balance.

4.The date passes

Once the offer has ended, the account can move onto the standard rate.

The problem is not awareness.

It is timing.

How Onremind protects the window before the price changes.

Add the date once. Onremind tracks the countdown, reminds you early, and gives you time to review, negotiate, cancel, switch or stay before the renewal date arrives.

Set the date

Add the renewal, expiry or contract-end date once.

Onremind keeps watch

Sit back. We quietly track the countdown for you.

Reminders during the action window

We remind you while there's still time to review and decide.

The date arrives

The renewal, expiry or contract-end date is reached.

Then the cycle begins again.

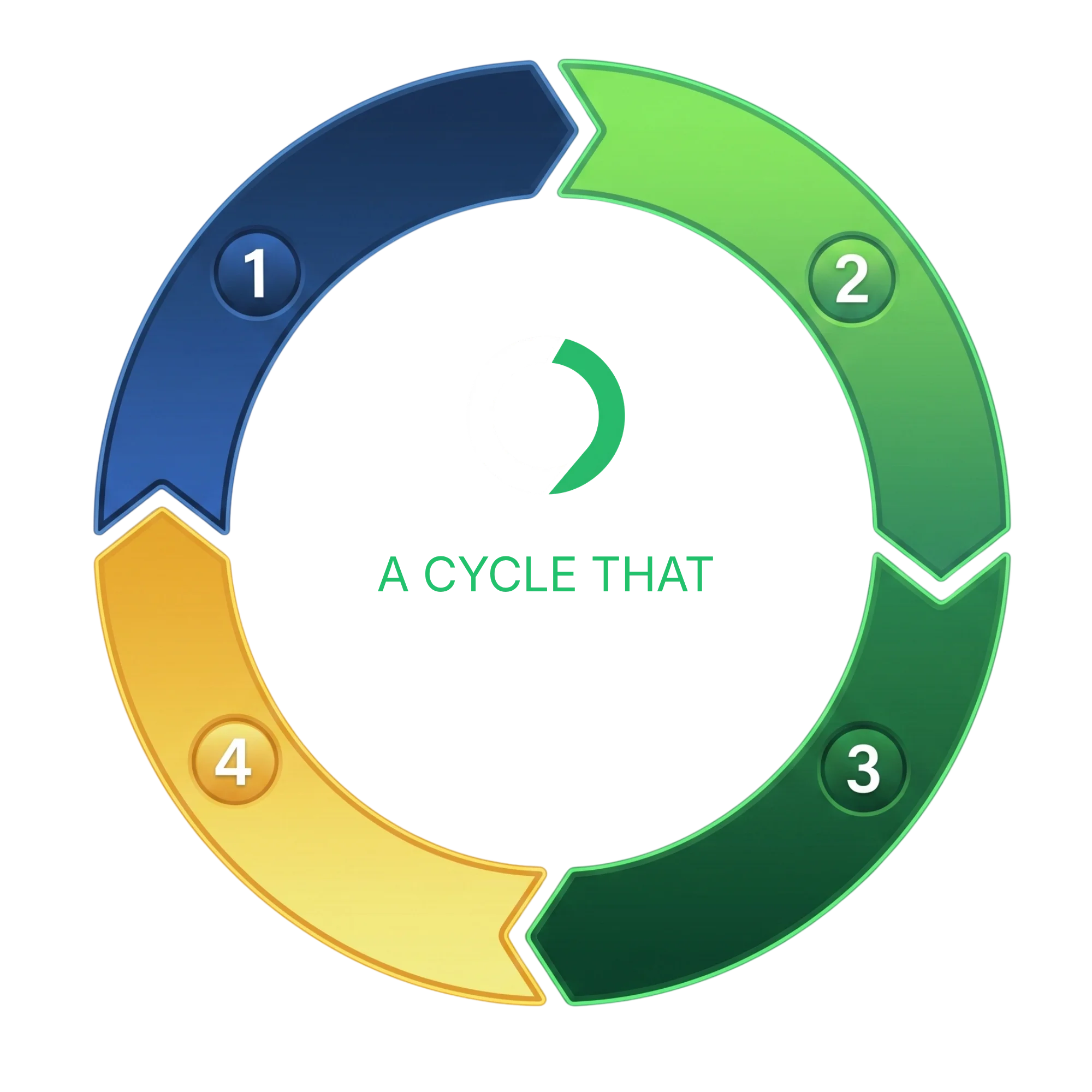

- 01

Set the date

Add the renewal, expiry or contract-end date once.

- 02

Onremind keeps watch

Sit back. We quietly track the countdown for you.

- 03

Reminders during the action window

We remind you while there's still time to review and decide.

- 04

The date arrives

The renewal, expiry or contract-end date is reached.

Then the cycle begins again.

- 01

Set the date

Add the renewal, expiry or contract-end date once.

- 02

Onremind keeps watch

Sit back. We quietly track the countdown for you.

- 03

Reminders during the action window

We remind you while there's still time to review and decide.

- 04

The date arrives

The renewal, expiry or contract-end date is reached.

Then the cycle begins again.

Onremind protects the time before the price changes — not after.

The renewal date is the trigger. The renewal action window is the time Onremind protects.

CREDIT CARD FAQS

Questions before you add a credit card offer end date

A few clear answers about how Onremind works for 0% and balance transfer offer endings.

Credit card offer guidance

Clear reports, guides and updates for the moments before 0% offers or balance transfer periods end and interest may apply.

Reports

Longer reads on renewal prices, market conditions and what to check before the date arrives.

Guides

Practical checks to make before a deal, tariff or subscription rolls on.

Updates

Recent regulator and market developments relevant to upcoming renewal dates.

Balance transfer deal ending: what it means before interest starts

January 2026

A balance transfer period ending is a real pricing trigger. Here is what it means before interest starts again.

0% credit card deal ending: what it means before interest starts

January 2026

A 0% credit card expiry is a real pricing trigger. Here is what it means before interest starts.